Financial Future: The Real-Time Race Between Banks, FinTech, and DeFi

If you’re wondering about the future of finance, Amazon’s growth over the last 30+ years provides a model of what’s possible.

On the one hand, the company is famous for its relentless focus on prioritizing customer experience, even at the expense of vendor relations and profit margins. This focus has delivered community reviews, free two-day shipping for Prime members, and the ability to complete purchases with one click/tap of a button.

But Amazon’s success also stems from a constant drive to disrupt traditional channels by removing inefficiency. From the outset, Jeff Bezos recognized massive amounts of time and energy built into 20th-century bookselling, from high margins to a retailer’s ability to “return” inventory.

Amazon leveraged the efficiencies of an emerging e-commerce model over brick-and-mortar retail. Then, it removed the inefficiencies of paper distribution and consumption with the Kindle Reader. Today, over one in five books sold is an ebook.

The company took those learnings and applied them to cloud computing resources, shipping, and supermarkets, and have even extended into pharmaceutical sales. Yet, the world still contains many inefficient legacy business models waiting to be displaced by modern, digitized alternative.

One of those legacy models is “modern” finance. If you’ve purchased or refinanced a home, you’ve experienced the stacks of forms that require signatures and initials — not to mention thousands of dollars of fees tacked on for paying various departments, offices, and intermediaries.

The U.S. Federal Reserve, despite running entirely automated computing systems, cannot settle transactions on weekends or holidays. Until recently, standard Automated Clearing House (ACH) funds transfers required five business days to settle, and even now, the norm remains one to two business days — and that’s only if your bank doesn’t place a hold on the funds (like the common practice of waiting up to seven business days to confirm a deposited check).

Why is this still happening in an age of real-time computation, encryption, databases, and transcontinental networking?

The answer lies in long-established and deeply rooted inefficiencies baked into the multi-trillion-dollar traditional finance (“TradFi”) industry. But, much like the Amazon disruption of retail stores, change is coming quickly to finance via multiple avenues, including the financial technology (FinTech), centralized finance (CeFi), and decentralized finance (DeFi) sectors.

Like paper books and shopping malls, legacy finance won’t disappear overnight, but the balance is already shifting rapidly, but banks do have a light at the end of the tunnel: real-time data.

TradFi: Settle Down

The contrast between legacy and future models for finance shows up clearly in how settlement periods operate.

Inter-bank settlement has roots that reach back to medieval times when the essential processes for clearing (calculating how much one bank owed another following multiple client transactions) and settlement (the exchange of assets to pay off obligations) were established.

Not surprisingly, moving gold or even certificates between banks proved difficult to scale — legacy inefficiencies go back a long way — and centralized “clearing houses” emerged to assist with clearing and settlement under a single roof. Clearing houses, in turn, evolved into nationalized central banking.

Short version: Money moves between people through layers of banks. The financial system has evolved rules that provide clearing and settlement time to ensure that sufficient funds move successfully through each layer.

Here’s how it works:

- In the TradFi system, when Party A sends money to Party B, the request moves through a settlement bank.

- This request sets off a series of events that result in Party A’s bank deducting the money from A’s account and Party B’s bank crediting that same amount of money to B’s account.

- No actual money changes hands. Instead, the tallies change in each bank’s respective settlement accounts, which are liquidity pools meant to accommodate the many interbank requests made every day.

- After the close of business, the banks conduct settlements with the centralized settlement bank.

In this situation, an actual settlement generally happens the business day after the transaction. ACH transfers take longer because they involve payment processors, merchants, two banks, and, in the middle of it all (in the U.S.), the Federal Reserve, which handles overnight processing. More layers mean more time, ostensibly in the name of mitigating risk and ensuring accuracy.

Traditional banks and financial institutions are facing disruption and are now looking to improve profitability by enabling customers to be served faster. In a system based in medieval times, they need to look towards technology to help retain customers in the battle with decentralized finance (that is far from over).

Real-Time Data Could be the Answer that Banks are Looking for

Real-time data is information that is delivered immediately after collection. This may seem antithetical to how banks operate, but it doesn't have to be; competing with decentralized finance will require banks to adopt a real-time position, especially as it relates to data.

A company that can help enable this is Redis.

As the company describes it, Redis can be “used as a database, cache, and message broker” through various data structures. Redis provides for on-disk persistence, asynchronous replication, high availability, and automatic partitioning. Most importantly for this discussion, Redis achieves its real-time results by keeping datasets in memory. With traditional data architectures, a subset of the application’s total dataset—typically the “hottest” or most immediately needed data—resides in DRAM-based system memory, while the majority of data sits in slower but much less expensive disk (and/or SSD) storage. In-memory architectures swallow the bitter pill of higher costs to avoid time-intensive fetching of data from high-capacity storage media.

In a previous article, we covered how Redis is enabling the future of AI, but an in-memory, multi-model database capable of sub-millisecond latency has applications across many businesses, including banks.

These institutions require true real-time data and high performance databases in order to serve customers as effortlessly their competitors can.

With the explosion of real-time trading, customers expect real-time data relating to their transactions, accounts, and any banking-related information.

Fintech Futures and Redis said exactly that in early 2021.

To take advantage of these opportunities, financial institutions require a high-performance database that delivers sub-millisecond response times for reads and writes, stores data from dozens of data sources in multiple data models, and provides high availability and multi-layered security.

At the core of Redis' value proposition for financial institutions is that it can reduce the complexity of delivering real-time data for all banking customers.

Currently, getting financial data to customers immediately is a tremendous challenge. Many banks have built their customer applications on top of relational databases. These types of databases were created during a time in which customers had minimal transactions and queries. Unfortunately, these databases are now constantly stressed (often beyond capacity) to accommodate the millions of customers constantly accessing their records and transacting with their accounts.

As a way to combat these issues, some banks have added a 'cache' to their relational databases and others have employed specialized database hardware applications. Both of these options are expensive, complex, and difficult to manage. A banking customer might care about these costly and complex "enhancements when charges are passed onto them in the form of increased banking fees, or when outages frequently occur.

Redis is a multi-model database, which means that a bank doesn't have to maintain separate databases for all of their various data models. This provides reduced complexity and overhead for banks, while enabling them to more easily meet the demands of their customers.

Specifically, RediSearch is a module that sits on top of Redis (both on premise and cloud instances) and acts as a text search and secondary indexing engine. This provides real-time data and an opportunity for banks to address customer needs immediately.

Redis also has the ability to aid institutional investors by reducing latency during trading. Redis Enterprise can process millions of data points per second, and again, on a sub-millisecond level. Portfolio managers are often analyzing thousands of potential trades a day and the validity of any of these trades can change in a matter of seconds. A solution that reduces latency can improve the returns of these traders.

Finally, real-time data not only improves customer data-access, but also the general security of a bank. RedisGraph can help find relationships between various transactions, and along with RedisBloom, which can help detect unusual account activity via probabilistic data structures, can detect fraud.

It's clear that traditional banks have an upward battle, but solutions like Redis can help make them more competitive in the face of increased competition.

FinTech: Trad on Speed

The model of FinTech represents what happens when you apply modern technology to traditional finance mechanisms. Depending on who you ask, it’s possible to trace FinTech’s starting point back to the telegraph’s invention in 1886. A more obvious origin story might be the creation of NASDAQ, the first digital stock exchange, following the Securities Acts Amendment of 1975.

However, end-to-end services digitalization didn’t arrive until the 21st century, and while FinTech can serve as an umbrella term referring to any finance mechanism using modern technology, there is a core element of legacy finance that remains important.

The bureaucracy and rules of traditional finance serve to establish trust between financial entities and settlement layers. Without trust, the financial system fails. The 2008 collapse and the subsequent role of monetary stimulus in propping up banks to re-establish public trust offers an excellent case study.

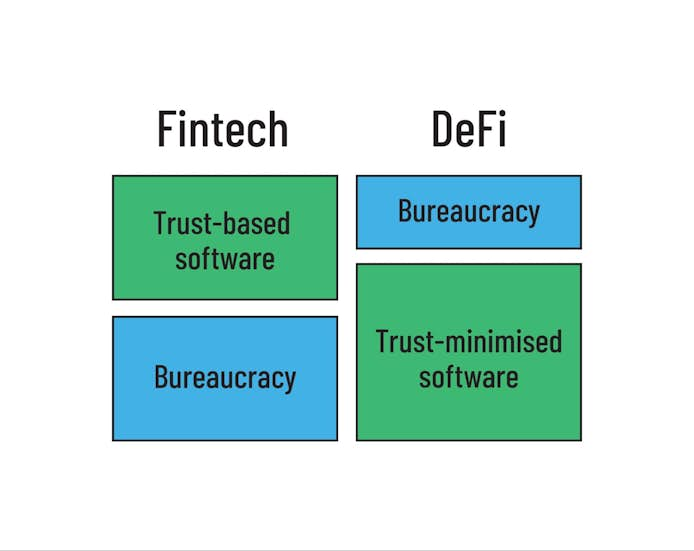

Long story short, FinTech maintains the infrastructure and bureaucracy of TradFi. But it replaces specific components of that system with trust-based software, as noted by Tobia De Angelis’s contrast of DeFi and FinTech.

You can think of it like a raceway constructed over a gravel road. Transactions zip along between beautiful software interfaces, but those vehicles can only stop (settle) by exiting onto the slow, dusty lane below. This is one reason why FinTech services such as PayPal and Venmo have faced minimal institutional or government oversight; they run on legacy rails and adhere to the traditional rulebook.

FinTech organizations reap the rewards of automation by implementing modern software and computer systems, including bringing artificial intelligence to bear on perennial challenges such as insurance, high-speed trading, and risk management. Similarly, real-time payment (RTP) solutions, which operate 24x7x365, replace that second-level raceway with FinTech teleportation pods. RTP enables instant settlement thanks to intermediaries such as Fiserv and PayFi.

So far, The Clearing House’s RTP remains America’s only fully operational RTP. FinTech services like PayPal, Venmo, and Zelle can provide real-time payments between bank accounts through integration with The Clearing House. Many merchants, banks, and billing organizations “anticipate customer service improvements” from RTP services.

How much is all of this worth? Around $159B, according to a 2020 T4 report, and it’s forecast to nearly double to $310B by 2022. A range of companies from Amazon to Goldman Sachs are adopting FinTech because enterprises must either adapt or die. Sixty percent of credit unions and 49% of banks in the U.S. believe that fintech partnership is essential, according to payment automation systems provider Tipalti.

In a January 2021 analyst conference call, Jamie Dimon, CEO of the #1 U.S. bank JPMorgan, was asked whether FinTech entities have “trounced” traditional banks in recent years and gave a telling answer...

“Absolutely, we should be scared about that…we’ve just got to get quicker, better, faster.”

DeFi and CeFi: It’s Time to Yield...Maybe

The titans of TradFi are correct to be scared, because as compelling as FinTech may be, cryptocurrencies and their associated decentralized finance (DeFi) and centralized finance (CeFi) services are poised to make an even more significant impact.

Banks and governments have fought the growth of cryptocurrency for years. For example, Dimon called Bitcoin a fraud in 2017 and threatened to dismiss any JPMorgan trader caught buying or selling it. Fast forward a few years, and JPMorgan now offers six crypto funds, one of which is based on the #2 blockchain, Ethereum.

BNY Mellon, Morgan Stanley, Wells Fargo, and U.S. Bank have all embraced cryptocurrency in various ways, too. TradFi institutions are starting to accept cryptocurrency as reliable financial vehicles. That’s a sweeping narrative change from the days of Dimon describing Bitcoin as “only for use by criminals and North Korea,” a sentiment still echoed by some prominent U.S. policymakers. Like the 1990s internet, crypto will endure years of misunderstanding, fear, and scorn before becoming the new, improved, and far more efficient routine.

DeFi Mechanics

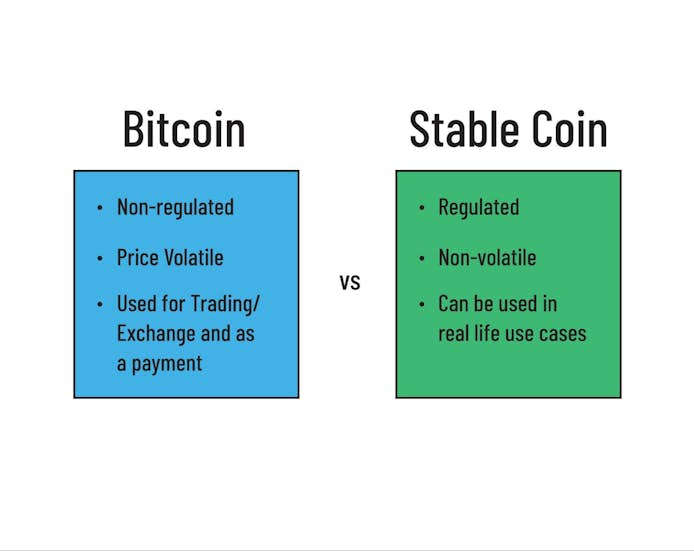

If you need an introduction or refresher on blockchain tech, there are useful overviews from Coingeek or Coindesk. But, for our purposes, the main point is that cryptographic blockchain networks like Bitcoin and Ethereum often incorporate coins/tokens able to function as stores of value and currency. In other words, cryptocurrencies do not operate on legacy TradFi rails. You can still use exchanges to convert fiat currencies, such as the U.S dollar or Euro, into cryptocurrencies, but the process adds complexity and cost. It’s like taking a ferry across the water separating two very different countries.

Stablecoins serve as a bridge between the two sides. Stablecoins are usually pegged on a 1:1 basis to a stable entity, such as the U.S. dollar. Most stablecoins maintain their stable value because they are backed by trusted collateral. Stablecoins are cryptographic assets that operate on crypto rails and can thus interact much more seamlessly with other cryptocurrencies, yet they exhibit the value stability of fiat currency.

This means that stablecoins provide a bridge between the fiat and crypto domains that is becoming increasingly important in DeFi, and may offer an easier route for TradFi institutions to transition into crypto services, as Visa demonstrated with its March 2021 announcement about settling payments in USDC stablecoins on the Ethereum blockchain.

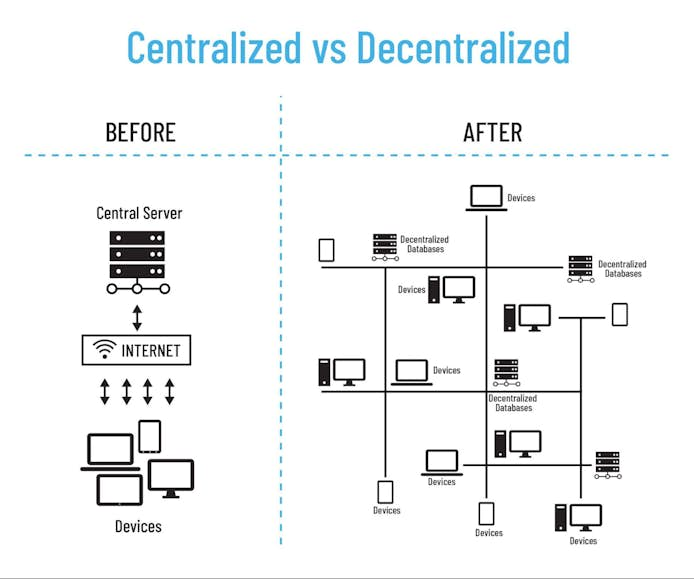

In DeFi, cryptographically secure blockchain technology is the root of trust instead of a centralized governmental authority or banking system. Most blockchains are globally distributed, censorship-resistant, and transparent, so assets and transactions can be audited by literally anyone. DeFi tools and services are also open sources, so anyone can build them without the need for licensing or permission. More importantly, DeFi is based on smart contracts, which are blockchain-based programs that follow if/then rules. There’s no delay from human intervention, ambiguous interpretation, or layers of go-betweens.

DeFi is quickly replicating many TradFi and even some FinTech offerings with higher efficiency. Lending, insurance, derivatives, futures, and much more are available today, with new services appearing constantly. DeFi is pure market Darwinism at work, and doesn’t need permission from anyone to operate. Those that earn the market’s trust and outperform their peers will survive.

Going back to the idea of trust, FinTech balances bureaucracy with trust-based software. DeFi is nearly all trustless software. TradFi and FinTech trust is based on the provider organization. That trust begins and ends with the organization’s human representatives and whatever shifting agendas they may have. With DeFi, trust is based on open software code and the laws of math and physics.

For those wanting a less demanding, more bank-like feel to their services, there’s also centralized finance (CeFi). CeFi organizations employ DeFi-like technologies and methods, but within the structure of a centralized business. Companies such as Coinbase, BlockFi, Celsius, Robinhood, and Gemini are prominent CeFi organizations.

They operate like banks or investment houses, complete with regulated know-your-customer (KYC) and anti-money laundering (AML) processes during customer account setup. Many crypto users gravitate to the ease and familiarity of CeFi, but this may change as DeFi services and interfaces continue to mature.

No wonder the net value locked in Ethereum DeFi was $3.18B on August 1, 2020, and $52.17B precisely one year later.

CeFi in Action

To illustrate the simplicity and advantage of these new systems, we procured a CeFi loan. Here’s how it worked:

- We posted Bitcoin assets into a CeFi account, where they earned a 6.25% annual yield while sitting idle.

- Using the service’s mobile app, we requested a loan against some of the Bitcoin assets, much as a TradFi loan might require a house as collateral.

- We selected a 25% loan-to-value option with a 1% annual interest rate with only a few clicks. (For every $25 borrowed, we had to post $100 of crypto as collateral.) Twenty-five cents of interest on that $25 borrowed, spread across 12 months, are due each year of the loan.

- Then, we submitted the loan request to the CeFi organization after dinner. The application took about two minutes to complete—no bank visits. No signatures. No papers. Two minutes.

- The loan was approved the following morning.

- Shortly after that, the loan appeared in our CeFi account in the form of USDC, as requested.

- We transferred the USDC to a different CeFi exchange, from which the USDC could be converted to U.S. dollars and transferred to a bank or used in other ways. The transfer settled in under 10 minutes.

- The entire loan process took under 12 hours.

Note that crypto assets can be sent anywhere in the world through the Internet, in any amount, almost instantaneously, and for nearly nothing in network fees. (Compare that to the multi-day, fee-laden process of sending remittances across borders with TradFi services like Western Union.)

D) All of the Above

TradFi has decades of refinement and stability under its belt. Despite its legacy baggage, it does things very well, including providing a safe home for the only currency usable for paying taxes. Bureaucracy and regulation ensure acceptance by the government, and that carries value.

FinTech offers similar benefits, but with more speed and flexibility, albeit sometimes at the expense of convenience (for example, you probably can’t buy groceries with Venmo or pay your taxes with Zelle).

DeFi/CeFi offers the cutting-edge speed and functionality of FinTech with many of the services of TradFi, but often at the cost (today) of mainstream acceptance and convenience.

Realistically, we will need all three models for the foreseeable future. TradFi and DeFi/CeFi may eventually absorb FinTech, and the lines between the two remaining models will blur at many points.

One clear thing is that users of these changing systems will reap more rewards and derive more value from their financial systems of choice than ever before.

All of the above requires investment in secure, performant networks as the race for global, real-time finance transactions goes faster and faster. While the public Internet was never built for those needs, a network like Subspace is ideal for tomorrow’s evolved finance services.

Subspace is releasing to the general public very shortly, sign up here and get ready to experience how our private internet can dramatically reduce latency, jitter, and packet loss for your real-time application.